Overview

With a strong healthcare infrastructure, highly skilled medical professionals, international standard medical services, and affordable healthcare costs, Thailand is a global hub for medical tourism. In 2019, approximately 3.5 million medical tourists visited Thailand. As of July 2021, the Joint Commission International (JCI) accredited 61 Thai medical institutes which offer all kinds of medical treatments, ranging from organ transplants to dental and cosmetic surgery. To focus on supporting infrastructure for medical tourism, Thailand is home to more than 38 thousand facilities that offer some form of healthcare services in the following distribution: private clinics: 24,800 (70%), public health and district health promotion center care facilities: 9,800 (28%), private hospitals: 370 (2%) and public hospitals: 290 (1%). Based on the Ministry of Public Health’s survey in 2019, most foreign tourists who received healthcare in Thailand did so through private hospitals.

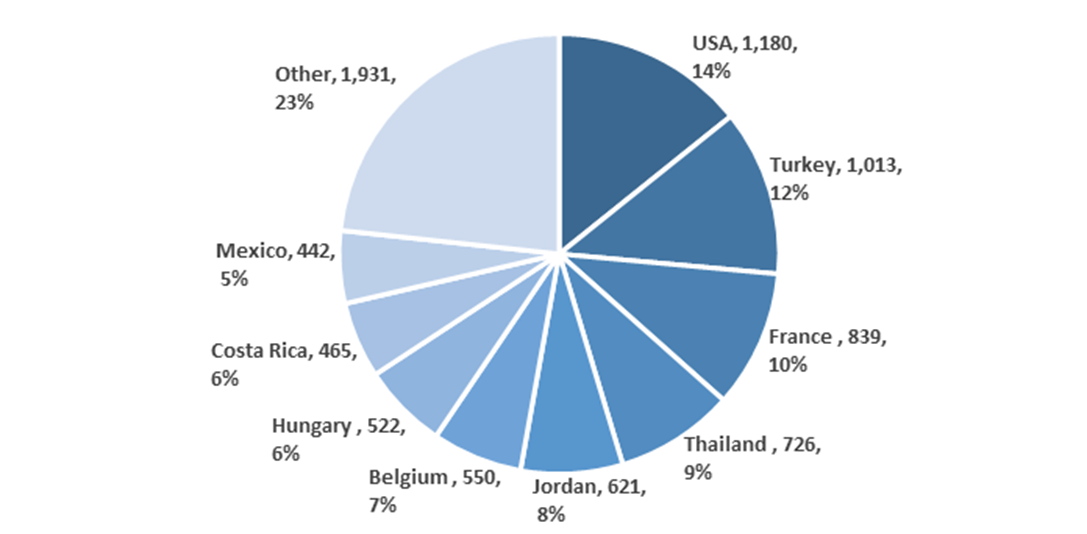

Figure 2. Destinations where International Medical Tourists were spending the most in 2019 ( USD Million, % of global total) Sources: IMF

Out of 118 nations in the IMF’s dataset, Thailand placed fourth in medical tourism spending overall and is the only Southeast Asian (SEA) nation to place in the top fifteen. Out of total inbound tourism spending in Thailand, which reached $58 billion in 2019, medical tourism spending accounted for one percent, which indicates the attractiveness of the Thai medical tourism sector.

Tourism has been a critical source of jobs and income for Thailand, and in 2019, a record 39.9 million tourists visited Thailand. Approximately 12-14 percent of Thailand’s gross domestic product comes from tourism. An economic contraction of six percent occurred in 2020, and hospitals supporting medical tourism have experienced direct adverse effects from the coronavirus epidemic.

In 2020, the value of Thailand’s medical device market was approximately $6 billion. In 2020, to cope with Covid-19, local manufacturers increased their production of personal protective equipment (PPE). Although imports of medical devices used for Covid-19 patients, such as ventilators, increased, imports of medical devices, in general, decreased by approximately 20 percent. That is because the majority of public and private hospitals have focused their budgets on Covid-19 treatment.

In April 2021, the Thai Food and Drug Administration (Thai FDA) issued new medical device regulations as part of an effort to align the country’s regulatory system with rules established in the ASEAN Medical Device Directive (AMDD). The new regulations require technical data for all medical devices: this data is to be submitted using the ASEAN Common Submission Dossier Template format.

Table: Medical Devices (Millions USD) Source: Medical Devices Intelligence Unit(MEDIU), Thailand Office of Industrial Economics

| 2018 | 2019 | 2020 | 2021 | |

| Total Local Production | 3,909 | 3,935 | 3,880 | 3,729 |

| Total Exports | 2,736 | 2,754 | 2,716 | 2,607 |

| Total Imports | 5,123 | 5,275 | 5.180 | 4,973 |

| Imports from the US | 712 | 784 | 731 | 702 |

| Total Market Size | 6,296 | 6,456 | 6,344 | 6,095 |

Leading Sub-Sectors

- Medical devices used to diagnose and treat COVID-19 include diagnostic tests, N95 masks, PPE coverall, sterilizers, ventilators, high flow oxygen therapy

- In vitro diagnostic devices (IVD) especially COVID-19 RT PCR tests, rapid antigen tests and antibody tests

- Health information technology, especially telemedicine and remote patient monitoring

- Cardiovascular devices

- Dental devices

- Dermatological devices

- Electro-diagnostic devices

- Neurological & surgical devices

- Ophthalmic and optical devices

- Orthopedic and fracture devices

- Rehabilitation equipment

- Therapeutic respiration devices

- Ultrasound and X-ray devices

Opportunities

The Covid-19 pandemic has accelerated the growth of telemedicine in Thailand. Large public hospitals, including Ramathibodi Hospital, Siriraj Hospital, and King Chulalongkorn Memorial Hospital, have developed and implemented their own telemedicine systems. Samitivej Hospital, part of the Bangkok Dusit Medical Services (BDMS) hospital chain, launched its virtual hospital to be accessed from a one-stop smartphone application, which is now an around-the-clock operation. Bumrungrad Hospital offers teleconsultation and remote patient monitoring for long-distance care for patients with arrhythmic heart conditions. Hospital providers have extended their services across borders. BDMS has partnered with Chinese platform Ping An Good Doctor, launching a joint operation at the end of 2019. The service allows patients in China to receive consultation from Thai doctors.

Thailand has an aging population, with 20 percent of its population forecasted to be over the age of 60 by 2022, increasing to 30 percent by 2035. This societal change is creating an imminent need for support services and facilities catering to an increasingly elderly population. Real estate developers are partnering with hospitals in developing senior care residence projects. Major public hospitals are developing their facilities to serve the elderly population. As a result, demand exists for related medical devices, products, and services for elder care.

The severely impacted economy has prompted Phuket to reposition the island as a world-class destination for health tourism. Phuket plans to construct an international medical tourism complex. The first development phase will include construction of four specialized medical treatment facilities – a general medical health center, a cardiac center, an international senior care facility, and a center for physical rehabilitation and anti-aging. In the second phase, three more specialized centers will be constructed, including the Bamrasnaradura Infectious Disease Institute headquarters, a Tropical Diseases Institute, and the Andaman Cancer Center. The new medical treatment complex in Phuket is expected to attract around 50,000 tourists in 2023 and one million by 2026.

Source: ITA